Compliance

FinCEN now requires reporting of all-cash residential property purchases by business entities or trusts to reveal beneficial owners and prevent money laundering. Strict penalties apply, with enforcement starting March 1, 2026.

FinCEN has appealed a recent federal court ruling that temporarily blocked the Corporate Transparency Act (CTA) and its Beneficial Ownership Information Reporting (BOIR) rules. Along with the appeal, FinCEN has requested an emergency stay to reverse the injunction and potentially reinstate the January 1, 2025, compliance deadline. If granted, businesses would need to comply with the reporting requirements, which include disclosing ownership details.

Nationwide injunction blocking enforcement of the Corporate Transparency Act (CTA) and FinCEN's Beneficial Ownership Information Reporting (BOIR) rules. The court ruled that these requirements overreach federal powers and impose unfair burdens on small businesses. While the injunction pauses the January 1, 2025, compliance deadline, FinCEN is expected to appeal and may seek a stay to reinstate the rules.

The Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury, enforces regulations to combat financial crimes in the United States.

With new BOIR compliance, LLCs and corporations must file reports detailing beneficial ownership to FInCEN.

FinCEN issues two types of IDs: one for reporting companies and another for individuals. It is important to understand important distinctions between the two.

The Financial Crimes Enforcement Network (FinCEN) safeguards the financial system against illicit activities using the Beneficial Ownership Information Reporting (BOIR) E-Filing System, enabling electronic submissions by financial entities. Users often face the "Invalid attachment" error, which occurs due to improper file formats (only JPG/JPEG, PNG, PDF accepted) or filenames with spaces/invalid characters. To resolve this, ensure files are correctly formatted and named.

The Corporate Transparency Act (CTA) mandates that LLCs and Corporations in the U.S. report detailed information about their beneficial owners and company applicants to FinCEN. This includes the full legal name, date of birth, residential or business address, and an identifying number from an acceptable ID document (such as a driver's license or passport), along with an image of the document.

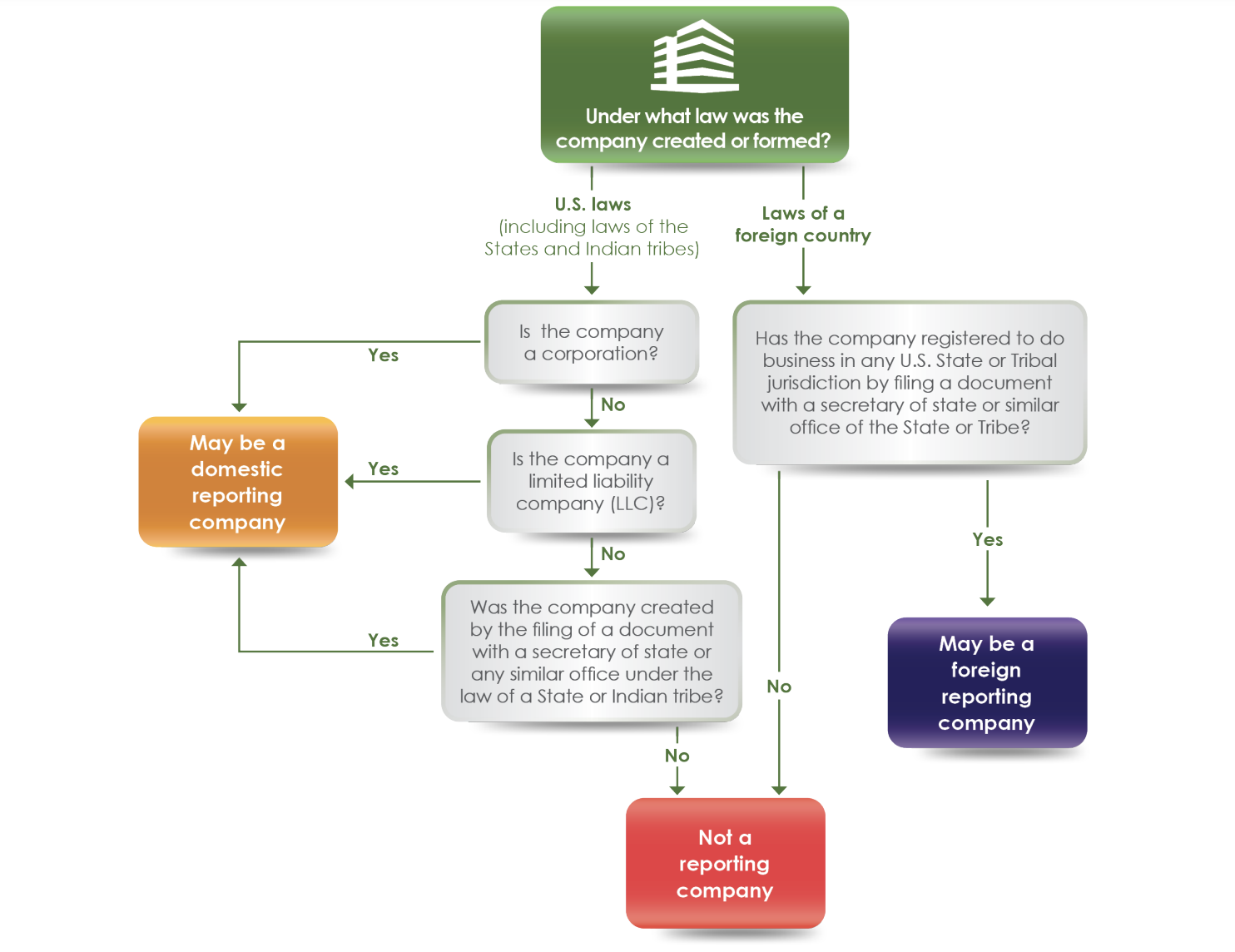

A "Reporting Company" includes most corporations and LLCs but exempts large operating companies, regulated entities, inactive entities, and certain nonprofits. Reporting Companies must provide detailed beneficial ownership information to FinCEN and update changes within 30 days.

The Corporate Transparency Act (CTA) requires U.S. companies to report their beneficial owners—those with substantial control or 25% ownership—to the Financial Crimes Enforcement Network (FinCEN) to combat financial crimes.

Reporting is mandatory by January 1, 2025, with updates within 30 days of changes. Entities dissolved before January 1, 2024, are exempt from reporting if the dissolution was formal and complete.

Administrative dissolutions do not exempt companies from reporting.

Compliance with the Corporate Transparency Act (CTA) in the U.S requires updating Beneficial Owner Information Reports with FinCEN.

Single-member LLCs and closely held corporations may only need a one-time report, but multi-member LLCs and corporations with multiple shareholders must continually update their beneficial owner information to avoid penalties of $500 per day, up to $10,000.

Changes in ownership, management, or personal details must be reported within 30 days.

U.S. citizens and residents are taxed on worldwide income under a unique system called citizenship-based taxation, which is only practiced by the U.S. and Eritrea.

The U.S. requires reporting of global income and compliance with complex rules like FATCA and FBAR. This system, known for its extensive reach, imposes significant reporting requirements and potential penalties for non-compliance.

Understanding these obligations is crucial for effective tax planning.